¿Cómo de difícil es invertir?

La mayoría de inversores profesionales no bate al mercado y la mayoría de inversores particulares pierde dinero. ¿Qué habilidades hacen falta para ser un inversor por encima de la media?

English version below

No descubro nada a nadie si digo que obtener rentabilidades mejores que el mercado de forma recurrente no es común. Es bien sabido en la comunidad inversora que la inmensa mayoría de gestores profesionales no es capaz de batir al mercado.

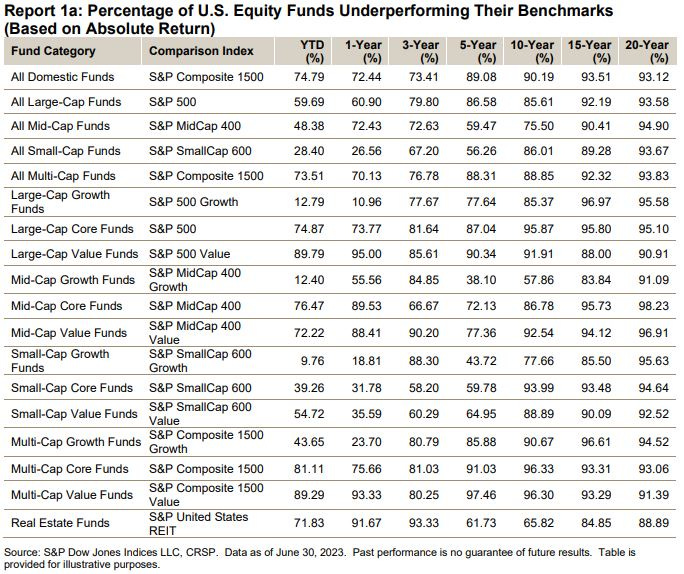

El índice Dow Jones publica anualmente un análisis de los retornos de los fondos de inversión de gestión activa, en comparación con los índices. He echado un vistazo al último informe publicado, que considera los primeros seis meses de 2023. Los datos son demoledores.

Vemos que hay alguna categoría de activos en los que un porcentaje considerable de fondos baten a su “benchmark” (mercado con el que se compara), si tomamos en consideración un horizonte temporal corto. Sin embargo, cuando nos vamos a las columnas de 10, 15 y 20 años, es una auténtica sangría. En general, menos del 10% de fondos baten al mercado en un periodo de tiempo significativo.

Evidentemente, este es un gran argumento para la inversión pasiva. Es el dato que suelen exponer los defensores de los fondos indexados. Y es normal, estoy de acuerdo con ellos. Si no quieres dolores de cabeza, y no tienes interés en gestionar activamente tu dinero, la cosa está clara: compra un par de fondos indexados de bajo coste y haz contribuciones periódicas de tus ahorros.

Pero este artículo no va de gestión pasiva, sino de cómo de difícil es ser un inversor mejor que la media.

Está claro, según los datos anteriores, que batir al mercado no es fácil. Hace falta un talento superior. Aquí me refiero a la definición de talento de Rafa Nadal, que me parece increíblemente certera. Nadal básicamente dice que el talento, en el tenis, es toda capacidad que te ayude a ganar: ya sea facilidad para hacer winners, resistencia, fortaleza mental o capacidad de trabajo. Aplicado a la inversión, es cualquier habilidad que te ayude a generar alpha (rentabilidad superior al mercado).

¿Cómo se puede llegar a ese rendimiento superior en la inversión? Principalmente, se puede resumir en dos categorías:

Capacidad de análisis: Hay quienes son capaces de ver lo que la mayoría de personas no ven. Algunos lo llaman pensamiento de segundo nivel, es decir, a la habilidad de llegar a conclusiones no evidentes a través de un proceso de razonamiento sofisticado. Esta capacidad permite identificar errores del mercado y apostar contra ellas con grandes retornos.

Howard Marks trata esta idea en su libro Lo Más Importante, en el que analiza las cualidades más importantes para un inversor. En él, dedica un capítulo entero al concepto de “pensamiento de segundo nivel”. En oposición al pensamiento de primer nivel, que es simplista, el pensamiento de segundo nivel tiene en cuenta más escenarios, más factores, asigna probabilidades… Los economistas pecan muy a menudo en pensamiento de primer nivel. Veamos un ejemplo práctico:

Problema: el precio de los alquileres es muy alto, la gente destina un porcentaje demasiado alto de su renta a ellos.

Ejemplo de pensamiento de primer nivel: los propietarios están siendo muy avariciosos, la solución es limitar el precio de los alquileres.

Ejemplo de pensamiento de segundo nivel: la limitación del precio de los alquileres haría que muchos propietarios sacaran sus viviendas del mercado de alquiler residencial y lo pusieran en alquiler vacacional, incrementando la escasez de alquileres residenciales y rentas todavía más altas; los propietarios han subido los alquileres en parte por el miedo a la ocupación, habría que legislar para dar seguridad a los propietarios; la oferta de vivienda en alquiler se ha mantenido estable y la demanda ha crecido, habría que favorecer el crecimiento de la oferta; etc.

Mientras el pensamiento de primer orden sólo considera lo que se ve a simple vista y no requiere mayor esfuerzo, el pensamiento de segundo orden contempla la segunda y tercera derivada, todas las variables posibles…, probabilidades de distintos escenarios… En definitiva, es más sofisticado.

En el mundo de la inversión, una buena forma de identificar pensamiento de primer orden es el test de “¿y quién no sabe esto?”. Se trata de cuestionarte si una una idea de una tesis de inversión es de conocimiento general. Por ejemplo: supón una tesis de inversión en una minera de litio que se basa en que la demanda futura de litio será alta por la importancia de este mineral en la producción de baterías de motores eléctricos, dado el actual contexto de descarbonización de la economía.

Este análisis es demasiado simplista. Cualquiera mínimamente informado sabe que el litio es un componente de las baterías eléctricas y que actualmente la tendencia es a desechar los combustibles fósiles. Lo más probable es que ese factor ya esté incluido en el precio, es decir, que ya lo descuente el mercado, y que ese razonamiento no vaya a reportar rentabilidades extraordinarias. En otras palabras: no hay alpha en las ideas simples, las grandes ideas de inversión son escasas, y llegar a ellas requiere lucidez y esfuerzo.

Capacidad de mantenerse racional: La facultad de ignorar la tendencia del mercado cuando ésta es claramente irracional. El mercado está enormemente influenciado por la psicología de los inversores. No voy a descubrir aquí que las personas actuamos de forma irracional constantemente. La psicología mueve los precios de los activos. Ello da lugar a burbujas y a precios ridículamente bajos. Aquellos que son capaces de no dejarse influenciar por las locuras del rebaño obtendrán retornos mejores a la media. Esta aptitud tiene más que ver con el estómago que con el cerebro.

Al final, ambas facultades se manifiestan externamente de forma idéntica: yendo en contra del consenso. Es lógico, ya que quien quiera batir al mercado tiene que hacer algo que no haga la mayoría.

¿Pero, cuál es el proceso de razonamiento interno que mueve al inversor superior a ir en contra del consenso? ¿Cómo se forman los mejores inversores el convencimiento de que una inversión merece la pena? O bien necesitas entender la realidad mejor que la media, o bien mayor templanza.

Veamos un ejemplo práctico de cada supuesto:

Empecemos por una inversión difícil de identificar:

En 2003, Amazon cotizaba a un precio de 1,07$ por acción. No había salido indemne del estallido de la burbuja “puntocom” y se había desplomado desde unos máximos cercanos a los 5,25$ por acción, una caída cercana al 80%.

Amazon era una pionera en el mercado de la distribución online. La primera dificultad de la tesis era reconocer el potencial de las ventas online. En 2003, el porcentaje de ventas por internet estaba por debajo del 2% de ventas totales en EEUU. Hoy, está cerca al 10%, lo que supone un crecimiento del mercado en torno a los 300 mil millones de dólares. Ese crecimiento parece muy obvio ahora, pero había que saber identificarlo en el momento, en un escenario de rechazo generalizado a todo lo relacionado con internet.

Además los fundamentales de Amazon tampoco eran espectaculares. En particular, presentaba unos márgenes muy malos. El primer año en que Amazon tuvo margen operativo positivo fue en 2002, con una beneficio operativo de 64 millones de dólares sobre unas ventas de casi 4 mil millones de dólares, lo que equivalía a un margen operativo de un 1,6%.

El principal motivo por el que Amazon tenía unos márgenes tan estrechos era porque gastaba una gran cantidad de dinero en I+D. El tratamiento contable de estos gastos es distinto en Europa y en EEUU y algo controvertido. La principal duda es si estos gastos se capitalizan (generando un activo en balance que se amortiza a lo largo del tiempo) o si se reconocen como gasto directamente. La principal diferencia es que si capitalizas estos gatos, el impacto en los beneficios se reparte a lo largo de la vida útil del activo reconocido a través del gasto por amortización. Si los das como gasto, toda la partida reduce tus ganancias en el ejercicio en el que incurras en ellos. En Estados Unidos, en general, estos gastos van a la cuenta de Pérdidas y Ganancias directamente, aminorando los beneficios. En definitiva, los gastos de I+D reducían ostensiblemente los márgenes de Amazon. Si obviabas estos gastos en el cálculo del beneficio operativo, los márgenes pasaban de 1,6% al 6,9% en 2002, y del 5,1% al 10% en 2003.

Vale, Amazon ganaba dinero, sólo que lo destinaba en grandes proporciones a I+D. Pero muchas empresas lo hacen, no sólo por eso ibas a pensar que Amazon fuera un chicharro. La clave aquí estaría en reconocer la estrategia de Bezos de consolidar una posición dominante en el mercado a través del gasto en innovación, unida al enorme viento de cola que supondría el crecimiento de las ventas online.

No hace falta que os diga que si hubieses invertido en Amazon en 2003, te habría ido bastante bien.

Veamos ahora el ejemplo “fácil”.

En el primer trimestre de 2020, al mercado le entró miedo por los posibles impactos de la pandemia del Covid y de las políticas de cuarentenas impuestas por la mayoría de Estados. Recuerdo artículos diciendo que era el fin de muchas industrias. Sí que es cierto que hubo muchas empresas que sufrieron y algunas quebraron, pero el miedo se contagió y se propagó irracionalmente a otras empresas y sectores más o menos ajenos a las consecuencias negativas de la pandemia. Un ejemplo clarísimo fue Apple, que cayó cerca de un 30% en marzo de 2020.

No hacía falta romperse la cabeza para saber que Apple iba a seguir vendiendo MacBooks, iPhones, Ipads, Airpods… Poco importaba que hubiera una pandemia global, encierros, cuarentenas o resquemor geopolítico hacia China. Da igual. La gente seguirá queriendo comprar los productos de Apple.

De hecho, la pandemia habría que interpretarla no como un problema, sino más bien como un viento de cola para Apple, dado el crecimiento de descargas de juegos móviles y otras aplicaciones en la Appstore, o el incremento de suscripciones a Apple TV procedente de toda la gente que no tenía mucho más que hacer que estar en casa y ver películas y jugar a videojuegos.

La acción de Apple creció aproximadamente un 230% desde marzo de 2020, lo que equivaldría a un rendimiento anualizado del 76%.

Ambas inversiones , tanto Amazon en 2003, como Apple en marzo de 2020, habrían generado rendimientos superiores al mercado. Sin embargo, el proceso necesario para llegar a cada una de ellas difiere mucho.

Para formarse convencimiento acerca de Amazon después de la burbuja “puntocom”, hacían falta conocimientos de contabilidad, un profundo entendimiento del modelo de negocio y de las fuerzas competitivas del sector del comercio online, así como de la estrategia de Bezos. En definitiva, una visión y capacidad de análisis considerables.

En cambio, cualquiera sabía que Apple iba a seguir liderando su mercado y siendo un excelente negocio durante muchos años, a pesar de que hubiera una, dos o tres pandemias. Para identificar esta oportunidad no hacía falta ser un visionario, ni un proceso de análisis muy sofisticado, sino levantar la mirada más allá del relato apocalíptico que dominaba el mercado.

No estoy diciendo que lo primero sea difícil y lo segundo fácil. Mantenerse racional en momentos en que prima la irracionalidad es harto complicado y requiere disciplina. Con respecto a la capacidad de análisis, hay parte innata y parte que se puede desarrollar, pero es algo que sólo tienen unos pocos (por supuesto, hay niveles).

Bien, hay inversiones más complejas que otras. Pero, ¿Cómo de difícil debe ser invertir la mayor parte del tiempo?

Merece la pena recordar el concepto de “círculo de competencia”, que tanto menciona Buffett. Los grandes inversores alcanzan una profundidad en sus análisis mucho mayor que el analista medio. Precisamente por ello, porque son conscientes de lo que requiere una idea de inversión ganadora, saben que no pueden alcanzar esa lucidez si no entienden todas las variables de una inversión. En una ocasión, a Buffett le preguntaron qué opinaba de Nike, y reconoció que no era capaz de saber quién sería el ganador en el mercado de las zapatillas deportivas. Él consideraba que ese negocio estaba fuera de su círculo de competencia y entender sus dinámicas demasiado complicado. Lo resumió con brillantez:

“Lo interesante de la inversión es que no son como los Juegos Olímpicos. No te dan puntos extra por el hecho de que algo sea muy difícil de hacer. Así que lo mejor es que saltes por encima de barras de un metro, en lugar de intentar saltar por encima de barras de dos metros”.

Esta cita me lleva a pensar que, dado que formarse convencimiento sobre una inversión requiere un gran conocimiento del negocio subyacente, sector, ventajas competitivas, equipo directivo y otras variables, los inversores han de limitarse a negocios que entiendan bien.

Por ejemplo, a nivel personal, como muchos otros inversores, tengo la norma de no tocar el sector financiero (ni aseguradoras ni bancos), por el simple hecho de que no creo que tuviera ninguna ventaja frente al analista medio a la hora de evaluar este tipo de negocios. Son demasiado difíciles para mí.

Utilizo la expresión “formarse convencimiento” de forma intencional. Para que una inversión sea exitosa no sólo vale con comprar una empresa que sea buena y vaya a dar buenos retornos, hay que tener convencimiento genuino. No vale de nada comprar una empresa que vaya a subir un 500% en 5 años si la vendes en el segundo año porque ha tenido una bajada momentánea de un 15%. Y al convencimiento sólo puede llegar uno mismo a través del análisis y del entendimiento.

El círculo de competencia te ayuda a eliminar complejidad a la inversión. No te hagas la vida más difícil de lo que ya es.

Al final, existe un punto medio entre complejidad y sencillez, que todo inversor debe perseguir. Para ser un gran inversor necesitas pensamiento de segundo orden y una elevada capacidad de análisis, pero también saber limitar la complejidad buscando negocios con ventajas competitivas fáciles de identificar a precios razonables. Además, en ocasiones, el mercado te dará oportunidades tan obvias que no necesitarás una visión especial para identificarlas, sino sólo ignorar la irracionalidad del mercado y mantenerte racional (de nuevo, es mas fácil decirlo que hacerlo).

Otro gran aliado del inversor es el largo plazo. El largo plazo nos permite diluir la importancia de nuestras valoraciones del precio de una acción, y que lo más importante sea el rendimiento del negocio. Si has comprado un gran negocio y lo mantienes en cartera durante muchos años, salvo que hayas pagado un múltiplo ridículamente alto por él, lo más probable es que obtengas una buena rentabilidad. Por ello, el largo plazo también puede ayudarnos a reducir la complejidad.

Al final, la clave para el inversor es minimizar al máximo la complejidad sin pecar de simplismo o pensamiento de primer orden. Einstein sintetizó esta idea de forma brillante: “todo debe hacerse lo más simple posible, pero no más simple que eso”.

En definitiva:

Las grandes ideas de inversión son escasas, y para llegar a ellas hace falta trabajo y capacidad de análisis.

Sin embargo, en ocasiones el mercado nos brinda oportunidades muy claras, que no requieren una gran capacidad de análisis e ingenio, sino un actuar racional cuando el mercado es irracional.

Los grandes inversores y las mejores ideas de inversión tienen ambos elementos: un gran análisis detrás y un precio irracional asignado por el mercado.

A pesar de la complejidad inherente a la inversión, los grandes inversores limitan esta complejidad limitándose a activos que entienden: mantenerse dentro de su círculo de competencia.

El largo plazo también ayuda al inversor a reducir la complejidad.

English version:

¿How hard is investing?

Most professional investors don't beat the market and most retail investors lose money. What skills does it take to be an above average investor?

I am not revealing anything to anyone if I say that outperforming the market on a recurring basis is uncommon. It is well known that the vast majority of professional managers are unable to beat the market.

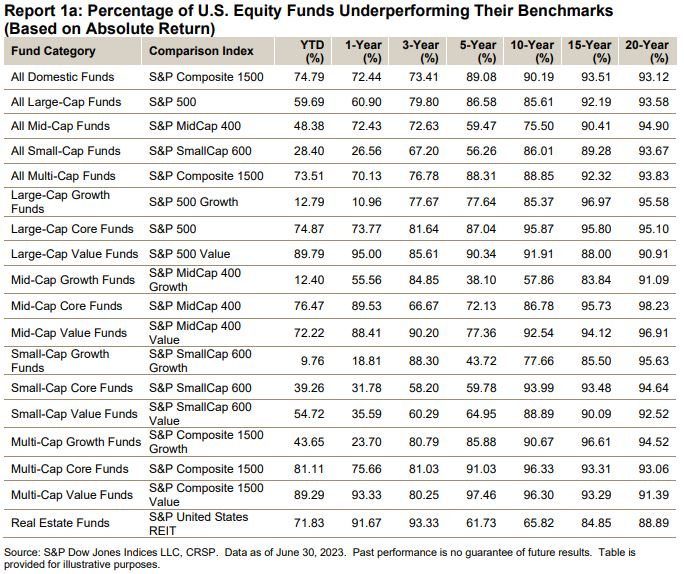

S&P Dow Jones Indices publishes an annual analysis of the returns of actively managed mutual funds compared to the indexes. I took a look at the latest report published, which looks at the first six months of 2023. The data is shattering.

We can see that there are some fund categories in which a considerable percentage of funds beat their benchmark if we consider a short time horizon. However, when we go to the 10, 15 and 20 years time-horizon columns, it is a bloodbath. In general, less than 10% of funds beat the market over a significant period of time.

Clearly, this is a great argument for passive investing. It is the fact that is often put forward by the advocates of index funds. And I get it, I agree with them. If you don't want headaches, and you have no interest in actively managing your money, just buy a couple of low-cost index funds and make regular contributions from your savings.

But this article is not about passive investing, but about how difficult it is to be a better-than-average investor.

It is clear from the above data that beating the market is not easy. It takes superior talent. By the way, I refer to Rafa Nadal's definition of talent, which I find incredibly accurate. Nadal basically says that talent, in tennis, is any ability that helps you win: whether it's the ability to make winners, stamina, mental toughness or work ethic. Applied to investing, it is any ability that helps you generate alpha.

How do you get to that outperformance in investing? Mainly, through two capabilities:

Analytical ability: there are those who are able to see what most people don't see. Some call it second-level thinking, i.e., the ability to reach non-obvious conclusions through a sophisticated reasoning process. This ability makes it possible to identify market errors and bet against them with large returns.

Howard Marks discusses this idea in his book The Most Important Thing, in which he analyzes the most important qualities for an investor. He devotes an entire chapter to the concept of "second-level thinking." As opposed to first-level thinking, which is simplistic, second-level thinking takes into account more scenarios, more factors, assigns probabilities... Economists very often are guilty of first-level thinking. Let's look at a practical example:

Problem: the price of rents is too high, people allocate too high a percentage of their income to them.

Example of first-level thinking: landlords are being too greedy, the solution is to limit rents.

Example of second-level thinking: limiting the price of rents would cause many owners to take their homes out of the residential rental market and put them into vacation rentals, increasing the shortage of residential rentals and increasing rents prices further; the supply of rental housing has remained stable and demand has grown, housing supply should be promoted...

While first-level thinking only considers what can be seen with the naked eye and does not require much effort, second-level thinking considers the second and third derivatives, all possible variables, probabilities of different scenarios... In short, it is more sophisticated.

In the investment world, a good way to identify first-level thinking is the "who doesn't know this?" test. It involves questioning whether an investment thesis idea is common knowledge. For example: suppose an investment thesis in a lithium mining company is based on the fact that future demand for lithium will be high because of the importance of this mineral in the production of electric motor batteries, given the current context of decarbonization of the economy.

This analysis is too simplistic. Any informed person knows that lithium is a component of electric batteries and that the current trend is to dispose of fossil fuels. Most likely, this factor is already included in the price, i.e. it is already discounted by the market, and this reasoning is not going to bring extraordinary returns. In other words: there is no alpha in simple ideas, great investment ideas are rare, and reaching them requires brightness and effort.

Ability to remain rational: The ability to ignore the market trend when it is clearly irrational. The market is greatly influenced by the psychology of investors. I am not going to discover here that people act irrationally all the time. Psychology drives asset prices. This results in bubbles and ridiculously low prices. Those who are able to not be swayed by the madness of the herd will get better than average returns. This aptitude has more to do with the stomach than the brain.

In the end, both abilities result in the same behaviour: going against the consensus. This is logical, since anyone who wants to beat the market has to do something that the majority does not do.

But what is the thinking process that drives the superior investor to go against the grain? How do the best investors build the conviction that an investment is worthwhile? Either you need a better-than-average understanding of reality or greater temperance.

Let's look at a practical example of each scenario:

Let's start with a difficult-to-identify investment:

In 2003, Amazon was trading at $1.07 per share. It had not emerged unscathed from the bursting of the dotcom bubble and had plummeted from highs near $5.25 per share, a drop of nearly 80%.

Amazon was a pioneer in the online distribution market. The first thesis difficulty was recognizing the potential of online sales. In 2003, the percentage of online sales was below 2% of total sales in the US. Today, it is close to 10%, which represents a market growth of around $300 billion. This growth seems very obvious now, but it was not that evident back then, in a scenario of generalized rejection of everything related to the Internet.

Amazon's fundamentals were not spectacular either. In particular, it had very poor margins. The first year in which Amazon had a positive operating margin was in 2002, with an operating profit of $64 million on sales of almost $4 billion, equivalent to an operating margin of 1.6%.

The main reason Amazon had such tight margins was because it spent a large amount of money on R&D. The accounting treatment of these expenses is different in Europe and the US and somewhat controversial. The main question is whether these expenses are capitalized (generating an asset on the balance sheet that is amortized over time) or whether they are recognized as an expense directly. The main difference is that if you capitalize these expenses, the impact on earnings is spread over the useful life of the asset recognized through the amortization expense. If you expense them, the entire item reduces your earnings in the year in which you incur them. In the U.S., in general, these expenses go directly to the income statement, reducing profits. In short, R&D expenses ostensibly reduced Amazon's margins. If you ignored these expenses in the operating profit calculation, margins went from 1.6% to 6.9% in 2002, and from 5.1% to 10% in 2003.

Okay, Amazon was making money, it was just putting it into R&D. But a lot of companies do that, so you wouldn't think Amazon was a winner just on that fact alone. The key here would be to recognize Bezos' strategy of consolidating a dominant market position through spending on innovation, coupled with the huge tailwind of online sales growth.

Needless to say, if you had invested in Amazon in 2003, you would have done quite well.

Now let's look at the "easy" example.

In the first quarter of 2020, the market was spooked by the possible impacts of the Covid-19 pandemic and the quarantine policies imposed by most states. I remember articles saying that it was the end of many industries. It is true that there were many companies that suffered and some went bankrupt, but the fear was contagious and spread irrationally to other companies and sectors that were more or less unaffected bythe negative consequences of the pandemic. A clear example was Apple, which fell nearly 30% in March 2020.

It was pretty obvious that Apple was going to continue selling MacBooks, iPhones, iPads, Airpods... It didn't matter if there was a global pandemic, lockups, quarantines or geopolitical resentment towards China. It doesn't matter. People will still want to buy Apple products.

In fact, the pandemic should be interpreted not as a problem, but rather as a tailwind for Apple, given the growth in downloads of mobile games and other apps in the Appstore, or the increase in Apple TV subscriptions from all the people who had little else to do but sit at home and watch movies and play video games.

Apple's stock grew approximately 230% since March 2020, which would equate to an annualized return of 76%.

Both Amazon in 2003 and Apple in March 2020, would have generated above-market returns. However, the thinking process required differs greatly.

To form a conviction about Amazon after the dotcom bubble required accounting expertise, a deep understanding of the business model and competitive forces in the online retail industry, as well as Bezos' strategy. In short, considerable vision and analytical skills.

By contrast, anyone knew that Apple was going to continue to lead its market and be an excellent business for many years to come, despite one, two or three pandemics. To identify this opportunity did not require a visionary, nor a very sophisticated analysis process, but rather to look beyond the apocalyptic narrative that dominated the market.

I am not saying that the former is difficult and the latter easy. Staying rational at a time when irrationality prevails is very complicated and requires discipline. With respect to the capacity for analysis, there is an innate part and a part that can be developed, but it is something that only a few have (of course, there are levels).

Well, there are investments that are more complex than others. But how difficult must it be to invest most of the time?

It is worth remembering the concept of the "circle of competence", which Buffett mentions so much. Great investors achieve much greater depth in their analysis than the average analyst. Precisely because of this, because they are aware of what a winning investment idea requires, they know that they cannot achieve that lucidity if they do not understand all the variables of an investment. Buffett was once asked what he thought of Nike, and he admitted that he could not tell who would be the winner in the sneaker market. He considered that business to be outside his circle of competence and understanding its dynamics too complicated. He summed it up brilliantly:

"The interesting thing about investing is that they're not like the Olympics. They don't give you extra points for the fact that something is very difficult to do. So you're better off jumping over one-meter bars, rather than trying to jump over two-meter bars."

This leads me to think that since building conviction about an investment requires a great deal of knowledge of the underlying business, industry, competitive advantages, management team and other variables, investors should limit themselves to businesses they understand well.

For example, on a personal level, like many other investors, I make it a rule not to touch the financial sector (neither insurance companies nor banks), for the simple fact that I don't think I have any edge over the average analyst in evaluating these types of businesses. They are too difficult for me.

I use the expression "building conviction" intentionally. For an investment to be successful, it is not enough to buy a company that is good and will yield good returns, you have to have genuine conviction. There is no point in buying a company that is going to rise 500% in 5 years if you sell it in the second year because it has had a momentary drop of 15%. And conviction can only be reached through analysis and understanding.

The circle of competence helps you to remove complexity from the investment. Don't make your life more difficult than it already is.

In the end, there is a middle ground between complexity and simplicity, which every investor should strive for. To be a great investor you need second-level thinking and a high analytical capacity, but you also need to know how to limit complexity by looking for businesses with easily identifiable competitive advantages at reasonable prices. In addition, sometimes the market will give you such obvious opportunities that you will not need special vision to identify them, but only to ignore the irrationality of the market and remain rational (again, easier said than done).

Another great ally of the investor is the long term. The long term allows us to dilute the importance of our valuations of the price of a stock, and that the most important thing is the performance of the business. If you have bought a great business and kept it in your portfolio for many years, unless you have paid a ridiculously high multiple for it, you are likely to make a good return. That's why the long term can also help us reduce complexity.

In the end, the key for the investor is to minimize complexity as much as possible without erring on the side of simplism or first-order thinking. Einstein synthesized this idea brilliantly:

"everything should be made as simple as possible, but no simpler than that."

Bottom line:

Great investment ideas are rare, and getting to them takes work and analytical skills.

However, sometimes the market provides us with very clear opportunities, which do not require a great capacity for analysis and ingenuity, but rather rational action when the market is irrational.

Great investors and the best investment ideas have both elements: great analysis behind them and an irrational price assigned by the market.

Despite the inherent complexity of investing, great investors limit this complexity by limiting themselves to assets they understand: staying within their circle of competence.

The long term also helps the investor reduce complexity.